Europe Artificial Intelligence as a Service (AIaaS) Market Summary

Europe’s Artificial Intelligence as a Service market was valued at USD 4.88 billion in 2024, is expected to reach USD 6.59 billion in 2025, and is projected to surge to USD 72.92 billion by 2033, growing at a strong CAGR of 35.05% (2025–2033).

Growth is driven by rapid cloud adoption, strict EU AI regulations, and rising demand for ready-to-use, compliant AI solutions across industries.

Market Valuation and Explosive Growth

The European AIaaS market is undergoing a massive transformation, shifting from an emerging sector to a core industrial pillar.

- Current Standing (2025): The market is valued at USD 6.59 billion as of 2025.

- Long-term Projection (2033): It is expected to reach a staggering USD 72.92 billion by 2033.

- Growth Velocity: The sector is expanding at a CAGR of 35.05%, driven by the rapid integration of AI into enterprise workflows.

Dominant Market Segments

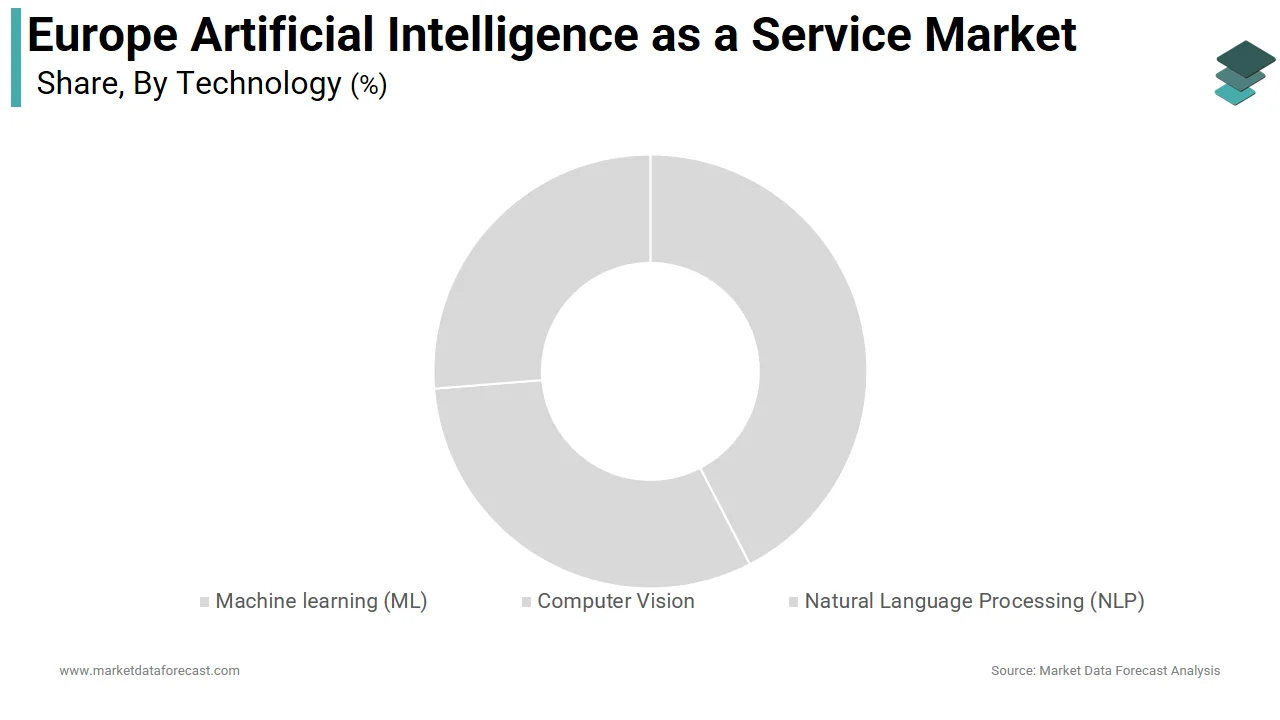

- Technology (Machine Learning): Machine Learning remains the backbone of the industry, commanding 65.5% of the market share. Its ability to provide predictive analytics and automation makes it the primary choice for European enterprises.

- Service Type (Software): The software segment is the most significant contributor, holding a 71% share. This highlights a trend where businesses prefer “plug-and-play” AI tools over building complex hardware infrastructures from scratch.

Regional Powerhouses

- Germany (The Leader): Holding 25.5% of the regional market, Germany is the central hub for AIaaS in Europe, largely due to its advanced manufacturing base and Industry 4.0 initiatives.

- The Netherlands (The Challenger): Noted for having the most promising growth potential (highest CAGR) due to its open-data culture, world-class logistics, and active participation in the GAIA-X sovereign data infrastructure project.

- UK & France: Both remain substantial contributors, with the UK leading in financial AI services and France in AI research and government-backed innovation.

Competitive Dynamics: “Compliance as a Competitive Edge”

Unlike the US or Asian markets, where raw scale often wins, the European market is defined by Strict Regulation and Trust.

- Regulatory Integration: Major players like Microsoft, Google Cloud, and IBM are winning by baking EU AI Act mandates (such as transparency and risk categorization) directly into their software architecture.

- The Rise of Sovereignty: European startups like Mistral AI are carving out niches by offering “Sovereign AI”—handling data within local borders and focusing on carbon-conscious computing.

- Sector-Specific Needs: In healthcare and finance, vendors are selected based on their ability to provide certified bias mitigation and clear audit trails for regulators.

Key Market Players

The market is a mix of global cloud hyperscalers and European industrial giants:

- Infrastructure & Cloud: Amazon Web Services (AWS), Microsoft, Google Cloud, and IBM.

- Enterprise Software: SAP SE, Salesforce, and Siemens.

- Specialized AI: Intel Corporation, BigML, and Fair Isaac Corporation (FICO).

Strategic Takeaway

The European AIaaS market rewards “Trustworthiness over just Sophistication.” In this environment, adherence to GDPR and GAIA-X alignment is not just a legal requirement but a fundamental design principle that determines market leadership.

Europe Artificial Intelligence as a Service Market Size

The Europe artificial intelligence as a service market was worth USD 4.88 billion in 2024, is forecast to reach USD 6.59 billion in 2025, and is expected to reach USD 72.92 billion by 2033, growing at a CAGR of 35.05% from 2025 to 2033.

Artificial Intelligence as a Service refers to cloud-delivered AI capabilities, including machine learning, natural language processing, computer vision, and predictive analytics, offered on a subscription or pay-per-use basis to enterprises, public institutions, and developers. Unlike embedded AI, this model enables rapid deployment without significant upfront investment in infrastructure or data science talent. The European AIaaS landscape is shaped by a confluence of digital transformation, stringent regulatory frameworks, and a growing pool of AI-ready data. In 2024, large European enterprises accelerated cloud‑based AI adoption, while the startup ecosystem expanded rapidly. The region’s data infrastructure underpins this growth, and the EU AI Act provides regulatory clarity that is reshaping how AI services are designed and consumed. This combination of enterprise uptake, ecosystem vitality, and governance is redefining how AI is integrated across the continent.

MARKET DRIVERS

Mandatory Compliance with the EU AI Act Accelerates Adoption of Certified AIaaS Solutions

The enforcement of the European Union AI Act has become a pivotal driver for AI as a Service adoption as organizations seek compliant readymade solutions to navigate complex regulatory obligations, which is majorly propelling the growth of the European AI as a service market. The law classifies AI systems into risk tiers and imposes strict transparency, data quality, and human oversight requirements, particularly for high-risk applications in healthcare recruitment and critical infrastructure. According to the European Data Protection Supervisor, over 75% of financial and healthcare institutions in the EU have deferred in-house AI development in favour of certified third-party AIaaS platforms that provide documented conformity assessments. Microsoft Azure AI and Google Cloud Vertex AI have both launched EU-specific compliance dashboards detailing data lineage model explainability and bias mitigation metrics aligned with ENISA guidelines. In 2024, SAP integrated its Joule AI assistant with built-in AI Act compliance checks, enabling customers in manufacturing and logistics to deploy predictive maintenance bots without legal exposure. As per the European Banking Federation, 60% of member banks now procure credit scoring and fraud detection AI exclusively through certified AIaaS providers to ensure audit readiness.

Shortage of In-House AI Talent Drives Reliance on Scalable Cloud-Based AI Platforms

Europe faces a significant deficit in specialized artificial intelligence professionals, compelling organizations to outsource model development and deployment through AI as a Service, which is further contributing to the regional market expansion. According to the European Centre for the Development of Vocational Training, the EU faced a shortfall of over 410,000 AI and data specialists in 2024, with Germany, France, and Italy accounting for nearly half the gap. This scarcity is most acute in small and medium enterprises, which lack resources to attract top data science talent. Consequently, 72% of European SMEs using AI rely entirely on cloud-based platforms, as per a 2024 Eurostat survey on digital business transformation. Providers such as IBM Watson and AWS SageMaker offer pre-trained models for demand forecasting, document processing, and customer sentiment analysis, requiring minimal coding. The French retail chain Carrefour reported reducing supply chain forecasting errors by 28% after implementing an AIaaS solution from Dataiku without hiring additional data scientists. Similarly, the Dutch healthcare provider Erasmus MC deployed an AI-powered radiology triage tool via Microsoft Azure in under eight weeks.

MARKET RESTRAINTS

Fragmented National Data Protection Regimes Increase Compliance Complexity for AIaaS Providers

Despite the EU AI Act’s harmonizing intent, the continued divergence in national data protection enforcement creates significant operational friction for AI as a Service vendors, which is hindering the artificial intelligence as a service market growth in Europe. While the General Data Protection Regulation provides a baseline, member states maintain independent supervisory authorities with varying interpretations of lawful AI training data use. According to the European Data Protection Board, enforcement actions against AI systems varied by a factor of three between countries in 2024, with Germany imposing strict consent requirements for biometric training data while Spain permitted broader public interest exceptions. This inconsistency forces AIaaS providers to maintain multiple data processing protocols even within a single cloud region. For example, an AI model trained on customer service transcripts may be deployable in Portugal but require re-engineering in Austria due to differing rulings on synthetic data validity. As per the European Consumer Organisation, 58% of AIaaS contracts now include country-specific addenda to address local data jurisprudence.

High Energy Consumption of Large AI Models Conflicts with EU Green Digital Targets

The computational intensity of generative AI and large language models poses a direct contradiction to the European Union’s Green Digital Compact, which mandates that digital transformation must align with climate neutrality goals, which is further impeding the expansion of the artificial intelligence as a service market in Europe. According to the Joint Research Centre, training a single large language model can consume over 1,200 megawatt hours of electricity, equivalent to the annual power use of 110 European households in 2024. Cloud providers offering AI as a Service are under mounting pressure to disclose and reduce the carbon footprint of inference workloads. The French data regulator CNIL now requires AIaaS vendors serving public agencies to submit energy efficiency certifications starting in 2025. Microsoft reported that its European AI workloads generated 320,000 metric tons of CO₂ equivalent in 2023, allocating €1.2 billion toward liquid-cooled AI data centers in Sweden and the Netherlands. However, smaller AIaaS firms lack such resources, with 67% unable to provide granular energy usage data, according to Tech Mahindra Europe.

MARKET OPPORTUNITIES

Integration of AIaaS into Public Sector Digital Services Unlocks New Institutional Demand

The European public sector’s digital modernization agenda is creating a structured pipeline for AI as a Service adoption across healthcare, education, and social services, which is a promising opportunity for the European artificial intelligence as a service market. According to the European Commission’s 2024 Public Sector AI Readiness Index, 23 out of 27 member states have active AI strategies incorporating cloud-based solutions for citizen services. In Estonia, the X Road data exchange platform now integrates AIaaS APIs for real-time benefit eligibility checks, reducing processing time from weeks to minutes. Similarly, Italy’s National Recovery and Resilience Plan allocated €1.4 billion to deploy AI-powered diagnostic support in 120 public hospitals using cloud-hosted models from NVIDIA and Philips. The European Health Data Space initiative further enables secure cross-border training of medical AI models on anonymized datasets hosted in GAIA X-compliant clouds. In 2024, the German Federal Employment Agency rolled out an AIaaS-powered job matching engine serving 5 million users annually with built-in bias detection certified under the EU AI Act.

Rise of Industry-Specific AI Model Marketplaces Fuels Vertical Specialization

A new ecosystem of vertical AI marketplaces is emerging in Europe, enabling domain-tailored AI as a Service offering that address sector specific data structures, regulatory constraints, and performance benchmarks, which is another notable opportunity for the regional market. Unlike generic cloud AI platforms, these marketplaces curate pre-validated models for discrete use cases such as crop yield prediction in agriculture or predictive maintenance in rail transport. According to the European Institute of Innovation and Technology, the AI4EU marketplace, launched in 2024, featured over 300 industry-certified models with 78% focused on manufacturing energy and mobility. Siemens’ AI Marketplace for Industry now offers 120 plug-and-play AI services for factory automation, all pre-audited for Machinery Regulation compliance. In agriculture, the Dutch startup GroenVision provides satellite-based pest detection AIaaS consumed by 1,200 farms through the Rabobank digital platform, with results validated by Wageningen University. As per Capgemini, 64% of European industrial firms prefer vertical AI marketplaces over horizontal cloud platforms due to higher accuracy and faster compliance.

MARKET CHALLENGES

Ambiguity in Liability Allocation for AI-Generated Outcomes Deters Enterprise Procurement

Despite regulatory advances, the European legal framework remains unclear on liability when AI as a Service output led to financial harm or safety incidents creating procurement hesitation among risk averse industries, which is one of the notable challenges to the European artificial intelligence as a service market. The EU AI Act assigns primary responsibility to providers of high-risk systems, yet operational control often resides with the deploying enterprise, leading to contractual disputes. According to the European Liability Directive Review Group, over 40 unresolved cases in 2024 involved conflicting interpretations of fault between AIaaS vendors and users. A German court ruling in March 2024 held a bank liable for loan denial errors from a third-party AIaaS tool, despite the vendor’s algorithmic disclaimer setting a concerning precedent. The European Insurance and Occupational Pensions Authority reports that only 29% of AIaaS contracts include clear indemnification clauses for algorithmic errors.

Vendor Lock-in Risks from Proprietary AI Model Formats Limit Interoperability and Portability

The lack of open standards for AI model packaging and inference interfaces in commercial AI as a Service platforms creates significant vendor lock-in risks for European enterprises, which further challenges the expansion of the European AI as a service market. Leading cloud providers use proprietary formats such as Amazon’s SageMaker Pipelines or Azure ML Workflows that are incompatible with competing ecosystems, requiring complete retraining for migration. According to ETSI, 82% of surveyed enterprises using multiple cloud AI services reported high costs and delays when attempting to switch providers in 2024. In the automotive sector, a major German OEM abandoned a pilot with Google Vertex AI after realizing its computer vision models could not be redeployed on its on-premise NVIDIA infrastructure without six months of redevelopment. The GAIA X initiative aims to address this through open AI interoperability specifications, yet adoption remains voluntary. The European Commission’s 2024 Cloud Rulebook identifies AI portability as a critical gap and proposes mandatory export formats for public sector contracts.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Technology, Service Type, Deployment, Organization Size, Vertical, Offering, and Country. |

|

Various Analyses Covered |

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Amazon Web Services, Inc., Salesforce, Inc., IBM Corporation, Intel Corporation, BigML, Inc., Fair Isaac Corporation, Microsoft, Google Cloud, SAP SE, Siemens, and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

The machine learning segment dominated the market by holding the largest share of 65.5% of the Europe AIaaS market in 2024. The dominance of the machine learning segment in the European market is attributed to its foundational role in predictive analytics, automation, and decision support across nearly all industry verticals. Organizations across finance, manufacturing, and logistics increasingly rely on machine learning as a service to transform historical data into actionable forecasts. As per the European Banking Federation, over 78% of European banks used cloud‑based ML models in 2024 for real‑time fraud detection and credit scoring. Similarly, Volkswagen integrated Azure Machine Learning across 26 plants, reducing unplanned downtime by 22%. A Capgemini study found that European enterprises using MLaaS achieved a 30% faster time to insight compared to in‑house development.

The computer vision segment is another promising segment and is predicted to witness a CAGR of 19.5% over the forecast period in the European artificial intelligence as a service market, owing to the rapid industrial automation and public safety mandates. European manufacturers are rapidly deploying computer vision as a service to automate inspection and enhance production line accuracy. Siemens reported that 85% of its German and Czech factories used cloud‑based CV models in 2024, achieving 99.6% defect detection accuracy. The European Factory of the Future initiative allocated €620 million in 2023 to support AI‑powered visual quality systems, with Bosch and Philips implementing real‑time defect detection on 200+ production lines. These systems process high‑resolution images at speeds exceeding 200 frames per second, leveraging GPU‑accelerated inference.

By Service Type Insights

The software segment led the market by occupying a 71% of the Europe AIaaS market share in 2024. The growth of the software segment in the European market is driven by the rising preference for self‑service, cloud‑based AI tools that integrate directly into enterprise workflows. The rise of low‑code AI platforms has democratized access to machine learning and natural language processing for business analysts and domain experts. Microsoft reported that over 250,000 European organizations used Power Platform with AI Builder in 2024 to create custom prediction models without writing code. Similarly, Google’s Vertex AI AutoML enabled retail chains like H&M to forecast seasonal demand using intuitive dashboards. A Forrester study found that 63% of European mid‑market firms adopted no‑code AI software to bypass data science talent shortages. The European Commission’s Digital Skills Partnership certified 120+ platforms in 2024 for alignment with AI literacy curricula, accelerating adoption in education and public administration.

The services segment is estimated to grow at the fastest CAGR in the European artificial intelligence as a service market during the forecast period, owing to the growing demand for customization and regulatory assurance. While off‑the‑shelf AI software offers speed, many enterprises require tailored solutions that reflect domain‑specific data structures and compliance requirements. In healthcare, providers such as IQVIA offer managed AI services that curate models for clinical trial matching using GDPR‑compliant data lakes. The European Health Data Space mandates strict secondary use protocols, prompting hospitals to outsource model validation to certified service partners. Similarly, the European Central Bank’s 2024 guidance on AI risk management led banks to engage Deloitte and Accenture for model governance audits. A McKinsey survey found that 58% of European enterprises using AIaaS procure supplementary consulting for bias testing and performance monitoring.

COUNTRY-LEVEL ANALYSIS

Germany Artificial Intelligence as a Service Market Analysis

Germany held the leading position in the European artificial intelligence as a service market in 2024 by accounting for 25.5% of the regional market share. The dominance of Germany in the European market is driven by industrial digitization, strong data protection norms, and public‑private AI initiatives. Germany’s AIaaS leadership stems from its Industrie 4.0 strategy, which mandates AI integration across manufacturing value chains. The Plattform Lernende Systeme national AI platform coordinates over 350 industry‑academia partnerships developing sector‑specific AI services. In 2024, SAP launched its Joule AI assistant embedded across S/4HANA, with over 18,000 German enterprises adopting it for supply chain and HR analytics. The country also hosts Europe’s largest GAIA‑X node in Frankfurt, enabling sovereign cloud AI with certified data rooms for automotive and chemical firms. Germany’s strict implementation of the Federal Data Protection Act ensures that only GDPR‑aligned AI services gain enterprise trust. The Ministry allocated €1.3 billion in 2024 to fund AI competence centers in Berlin, Munich, and Dresden, focusing on certified AI for critical infrastructure.

France Artificial Intelligence as a Service Market Analysis

France accounted for a promising share of the European artificial intelligence as a service market in 2024. This reflects its state‑led AI strategy and vibrant startup ecosystem. France’s AIaaS growth is propelled by the national AI strategy “AI for Humanity”, which mobilized over €2 billion in public investment since 2021. The country hosts 19 AI excellence institutes, including MIAI in Grenoble, which collaborates with Thales and Orange on secure AI services for defense and telecom. In 2024, the French Data Protection Authority certified 42 AIaaS platforms for public sector use, including Mistral AI’s language models for administrative automation. The aerospace giant Airbus uses AI services from Dataiku to optimize wing assembly with real‑time anomaly detection. France’s sovereign cloud initiative “Cloud de Confiance” mandates that all government AI workloads run on certified platforms, ensuring a stable demand base.

United Kingdom Artificial Intelligence as a Service Market Analysis

The United Kingdom is anticipated to command a substantial share of the European artificial intelligence as a service market during the forecast period. Despite post‑Brexit regulatory divergence, this reflects its deep tech talent pool and financial sector leadership. The UK’s AIaaS strength lies in its concentration of AI research institutions and fintech innovation. London hosts 38% of Europe’s AI venture capital, as per Tech Nation. Firms like BenevolentAI and Faculty AI provide specialized services in drug discovery and intelligence analytics. The Bank of England’s 2024 AI governance framework requires financial institutions to use third‑party validated models for credit risk, prompting widespread adoption of AIaaS from vendors like Faculty and H2O.ai. The National Health Service partnered with Microsoft to deploy an AI service for radiology triage across 35 hospitals, reducing reporting delays by 40%.

Netherlands Artificial Intelligence as a Service Market Analysis

The Netherlands is expected to exhibit a prominent CAGR in the European artificial intelligence as a service market during the forecast period, owing to its open data culture, logistics leadership, and GAIA‑X participation. The Netherlands excels in AIaaS deployment through world‑class digital infrastructure and collaborative data ecosystems. The National AI Coalition unites Philips, ASML, and Rabobank to develop sector‑specific AI services with shared data foundations. In 2024, the Port of Rotterdam implemented an AIaaS platform from IBM to predict vessel arrival times and optimize crane scheduling, cutting turnaround by 17%. The government’s “Data Sharing for AI” initiative provides legal templates for secure data pooling, enabling startups like Scailyte to train medical AI models on federated hospital data. Amsterdam hosts Europe’s largest data center cluster, ensuring low‑latency AI inference. The Netherlands Authority for Consumers and Markets certified 28 AI services with the “AI Proof” label in 2024.

Sweden Artificial Intelligence as a Service Market Analysis

Sweden is projected to hold a notable share of the European artificial intelligence as a service market during the forecast period, owing to its leadership in ethical AI innovation and green tech alignment. Sweden’s AIaaS market is distinguished by its emphasis on sustainability, transparency, and public sector digitization. The Wallenberg AI Autonomous Systems and Software Program has invested 3 billion SEK since 2018 in responsible AI research, with spin‑offs like Peltarion offering carbon‑aware AI training services. In 2024, the Swedish Social Insurance Agency deployed an AIaaS solution from IFS to automate parental benefit processing with real‑time bias monitoring. Ericsson uses AI services from AIMS API to optimize 5G network energy consumption, reducing base station power use by 22%. Sweden’s participation in the Nordic AI Alliance ensures cross‑border data sharing under strict ethical guidelines. The Swedish Data Protection Authority pioneered the “Algorithmic Impact Assessment” template, now adopted by 12 European countries.

COMPETITIVE LANDSCAPE

Competition in the Europe artificial intelligence as a service market is defined by a strategic race among global cloud hyperscalers to align technical capabilities with the region’s stringent ethical and legal standards. Unlike other regions where performance and scale dominate the contest in Europe, compliance, innovation, and trust are paramount. Microsoft, Google Cloud, and IBM lead by integrating EU AI Act mandates such as risk categorization, human oversight, and transparency directly into their service architecture. At the same time, European startups like Mistral AI and Peltarion carve niches through sovereign data handling domain expertise and carbon-conscious AI. The market is further segmented by industry, with healthcare and finance favoring vendors offering certified bias mitigation and audit trails. Public procurement rules increasingly require GAIA X alignment and GDPR compliant data processing, pushing vendors to localize infrastructure. Independent AI ethics auditors and national regulators act as de facto gatekeepers, influencing enterprise selection. This environment rewards vendors who treat regulation not as a constraint but as a design principle, resulting in a competitive landscape where trustworthiness equals technological sophistication.

KEY MARKET PLAYERS

The leading companies operating in the Europe artificial intelligence as a service market include:

- Amazon Web Services, Inc.

- Salesforce, Inc.

- IBM Corporation

- Intel Corporation

- BigML, Inc.

- Fair Isaac Corporation

- Microsoft

- Google Cloud

- SAP SE

- Siemens

TOP PLAYERS IN THE MARKET

- Microsoft is a global leader in artificial intelligence as a service with deep integration across its Azure cloud platform, offering a comprehensive suite of AI tools, including Azure Machine Learning, Cognitive Services, and the Copilot stack. In Europe, Microsoft has prioritized regulatory alignment by embedding EU AI Act compliance features such as model cards, data lineage tracking, and bias detection directly into its AI services. The company launched the Azure AI Governance Toolkit in early 2024, enabling European enterprises to conduct automated conformity assessments. Microsoft also expanded its sovereign cloud regions in Germany and Switzerland to address data residency requirements. Through partnerships with SAP Siemens and the European Health Data Space, Microsoft provides industry-specific AI solutions that meet both technical and legal standards, reinforcing its position as a trusted AI infrastructure provider across the continent.

- Google Cloud delivers advanced artificial intelligence as a service through its Vertex AI platform, which unifies machine learning, computer vision, and large language model capabilities in a single managed environment. In Europe, Google has focused on responsible AI by implementing the EU’s trustworthy AI assessment framework into its model deployment pipeline. In 2024, the company introduced the Vertex AI Regulatory Suite, featuring pre-built templates for high-risk use cases in finance, healthcare, and recruitment. Google also established an AI Readiness Program with France, Germany, and the Netherlands to train public sector developers on compliant AI deployment. Its partnership with CERN and ESA enables scientific AI services using European research data while maintaining GDPR adherence. These initiatives position Google Cloud as a technically robust and ethically grounded AIaaS provider in the region.

- IBM offers artificial intelligence as a service through its WatsonX platform, emphasizing explainability governance and industry specialization, particularly in regulated sectors. In Europe, IBM has distinguished itself by embedding AI FactSheets and automated risk classification aligned with the EU AI Act into all WatsonX services. The company launched the European AI Ethics Lab in 2024 in collaboration with the Technical University of Munich to validate fairness and transparency in AI models used by banks, insurers, and healthcare providers. IBM also integrated WatsonX with SAP and Salesforce ecosystems through certified connectors, enabling seamless deployment in enterprise workflows. Its hybrid cloud approach allows European organizations to run sensitive AI workloads on premises while leveraging cloud-based model training. This balance of innovation, compliance, and flexibility strengthens IBM’s role as a strategic AI partner for mission-critical applications.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe artificial intelligence as a service market prioritize regulatory compliance by embedding EU AI Act requirements directly into their platforms through automated risk classification, bias detection, and documentation tools. They invest in sovereign cloud infrastructure with localized data centers in Germany, France, and Switzerland to meet data residency and security mandates. Companies develop industry specific AI solutions for healthcare finance and manufacturing with pre validated models that accelerate deployment while ensuring domain relevance. Strategic partnerships with European enterprises, public agencies, and research institutions enhance credibility and co-innovation. Vendors offer AI governance toolkits and compliance dashboards as standard features to reduce customer burden. They also provide low-code and no-code interfaces to democratize AI access among non-technical users. Continuous investment in energy-efficient AI training and inference aligns with the EU Green Digital Compact. These strategies collectively address Europe’s unique blend of innovation, ambition, and regulatory vigilance.

MARKET SEGMENTATION

This research report on the Europe artificial intelligence as a service market has been segmented and sub-segmented into the following categories.

By Technology

- Machine learning (ML)

- Computer Vision

- Natural Language Processing (NLP)

By Service Type

- Software

- Data Storage and Archiving

- Modeler and Processing

- Cloud and Web-Based Application Programming Interface (APIs)

- Others

- Services

By Deployment

By Organization Size

By Vertical

- BFSI

- Healthcare and Life Sciences

- Retail

- IT & Telecommunication

- BFSI

- Manufacturing

- Energy & Utility

- Others

By Offering

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

link